Term Life Insurance: Secure Your Family's Future Today

Term life insurance provides coverage for a specific period and pays out a death benefit if the insured passes away during that term. It is a cost-effective way to ensure financial protection for loved ones.

Term life insurance offers budget-friendly premiums and straightforward coverage without cash value accumulation. This type of insurance is ideal for covering temporary needs like mortgages or debts that you want to protect your dependents from. Unlike whole life insurance, term life insurance does not provide coverage for the entire lifetime but offers a simpler and more affordable option for those looking for short-term financial security.

Introduction To Term Life Insurance

Term life insurance provides essential coverage for a specified period, offering immediate benefits to your family in the event of your passing. This type of insurance is budget-friendly and does not require a medical exam for approval. It is a smart choice for those with time-bound financial responsibilities, such as mortgages or tuition fees. However, it is important to note that once the term expires, the coverage ends, and no benefits are payable. Unlike whole life insurance, term life insurance does not accumulate cash value over time. It is crucial to weigh the pros and cons of each type of insurance to make an informed decision based on your individual needs.

How Term Life Insurance Works

Term life insurance provides coverage for a specific period of time, typically ranging from 10 to 30 years. The policy structure and terms may vary depending on the insurance provider. Premiums are based on factors such as age, health, and lifestyle habits. In the event of the policyholder's death during the term, the beneficiaries receive a payout, which is typically a lump sum payment. The payout process is straightforward and can usually be completed within a few weeks. However, if the policyholder dies within the first two years of the policy, the insurance company may investigate the cause of death to ensure that it was not a result of fraud or misrepresentation. While term life insurance does not accumulate cash value like permanent life insurance policies, it can provide affordable coverage for a specific period of time.

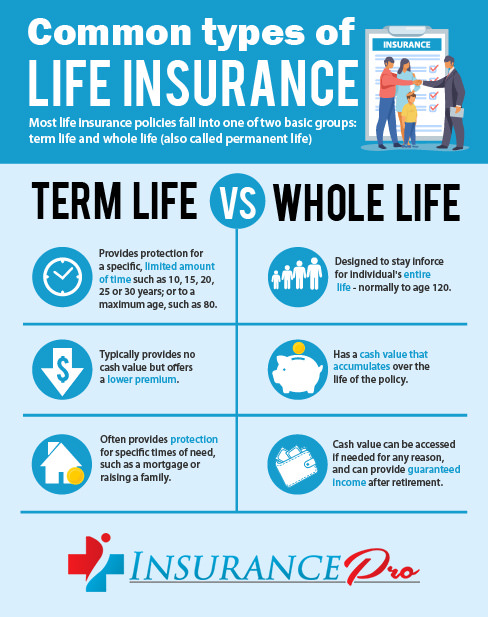

Comparing Term Life To Whole Life Insurance

When comparing term life to whole life insurance, it's important to consider the cost differences. Term life insurance typically offers lower premiums compared to whole life insurance, making it a more affordable option for many individuals. Additionally, the coverage duration of term life insurance is limited to a specific term, such as 10, 20, or 30 years, while whole life insurance provides coverage for the entire lifetime of the insured.

Another factor to consider is the cash value benefits. Whole life insurance policies accumulate cash value over time, which can be accessed by the policyholder. On the other hand, term life insurance does not offer cash value benefits, as it is designed to provide coverage for a specific term without any investment component.

Credit: insuranceprofl.com

Financial Security For Your Family

Ensure your family's financial security with Term Life Insurance, a budget-friendly option that provides coverage without medical exams. Safeguard your loved ones with monthly premiums designed to fit your budget and offer peace of mind for the future.

| Term Life Insurance provides financial security for your family. |

| It offers debt coverage and helps with education and daily living expenses. |

Determining Your Insurance Needs

To determine your insurance needs for term life insurance, consider your financial obligations and the length of coverage you require. Term life insurance provides a financial safety net for a specified period, offering affordable premiums and peace of mind for your loved ones.

It's a valuable option for covering specific financial responsibilities in the event of your passing.

| When determining your insurance needs, assess your financial situation carefully. Consider choosing the right policy term that aligns with your goals and budget. It's important to understand the coverage and benefits provided by term life insurance policies. Compare different options available in the market to find the most suitable plan for your needs. |

:max_bytes(150000):strip_icc()/dotdash-term-life-vs-whole-life-5075430-Final-60fb4e8f7bae43e0a65a3fac2431479c.jpg)

Credit: www.investopedia.com

The Application Process

Applying for term life insurance is simple and convenient. With online applications and no medical exams, it's easy to get budget-friendly coverage tailored to your needs. Secure your family's future with term life insurance today.

| The Application Process |

| Applying for term life insurance involves several important steps. Firstly, you'll need to complete an application form, providing personal and beneficiary details. Additionally, you may need to submit required documents such as identification and financial records. Some policies may require medical exams to assess your health, although there are exceptions for certain individuals. It's essential to understand the specific requirements of the policy you are applying for. Being prepared with the necessary documentation and information can streamline the application process and help you secure the coverage you need for your loved ones. |

Costs And Premiums

When considering term life insurance, it's important to factor in costs and premiums. Term policies offer budget-friendly coverage with fixed monthly premiums, providing financial security for your loved ones in case of an unforeseen event.

Credit: www.policygenius.com

Choosing The Right Insurance Provider

When selecting a term life insurance provider, it's crucial to consider their reputation and reliability. Look for companies with a strong track record of fulfilling their obligations to policyholders. Additionally, compare quotes and services from different providers to ensure you're getting the best coverage for your needs and budget.

Frequently Asked Questions

How Does A Term Life Insurance Work?

Term life insurance provides coverage for a specific period, offering a death benefit to beneficiaries. Monthly premiums ensure coverage.

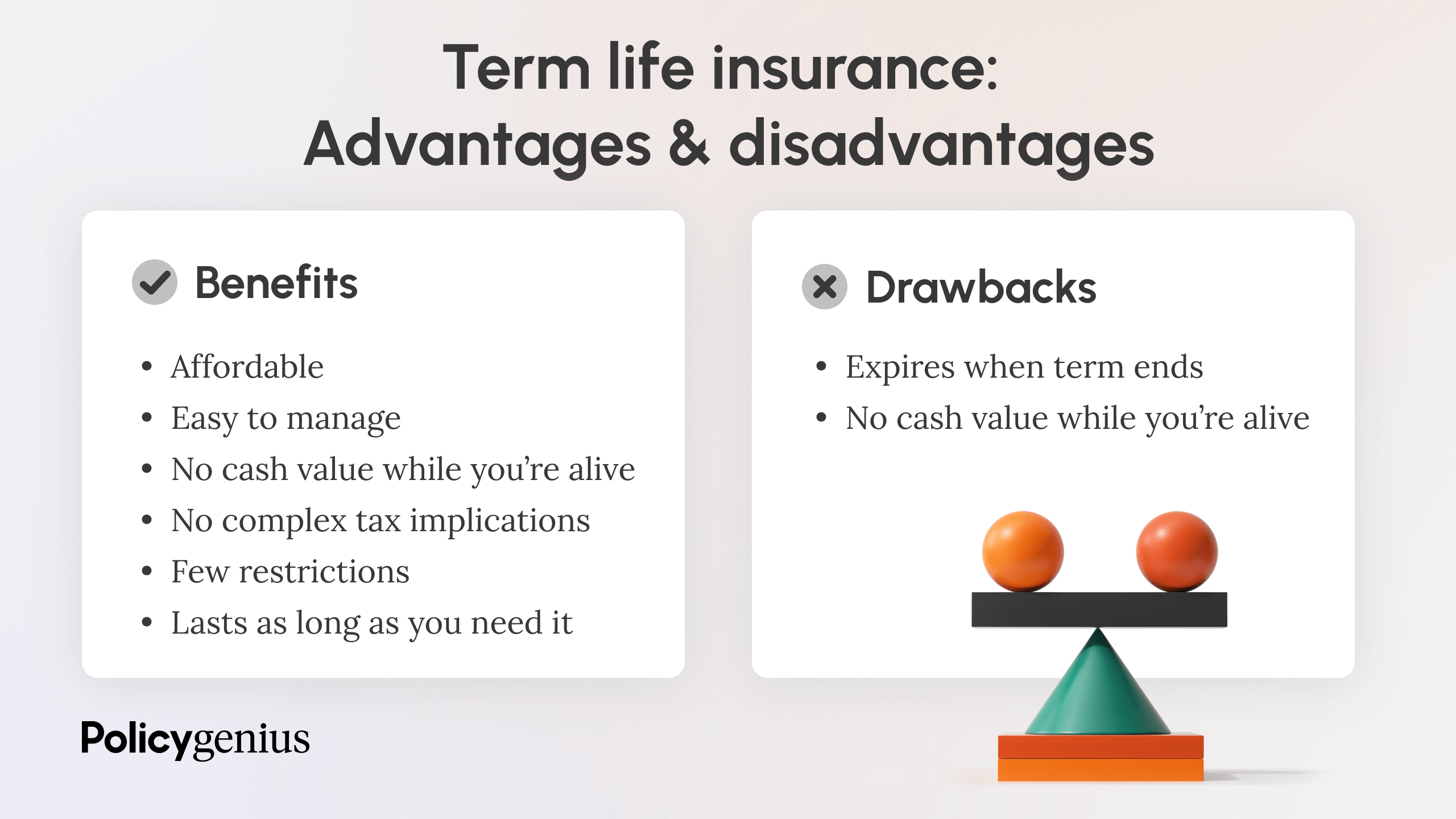

What Is The Main Disadvantage Of Term Life Insurance?

The main disadvantage of term life insurance is that coverage ends if you outlive the term.

Is It Worth Having Term Life Insurance?

Term life insurance is worth it when you have financial obligations like a mortgage or debt. It ensures your dependents can afford these expenses if you pass away. This type of insurance is affordable and straightforward, providing coverage for a specific period.

Which Is Better, Term Life Or Whole Life Insurance?

Both term life and whole life insurance have their own pros and cons. Term life insurance is more affordable and simpler, but it only provides coverage for a specific term and does not include a cash value feature. Whole life insurance is more expensive and complex, but it provides lifelong coverage and builds cash value over time.

The choice between the two depends on your individual needs and financial goals.

Conclusion

Term life insurance offers budget-friendly coverage with no medical exams required. It's a smart choice for ensuring your dependents can afford debts and time-boxed expenses. While it lacks a cash value feature, it provides a guaranteed life benefit for beneficiaries.

Consider your needs and options carefully.